Learn About The Law

Get help with your legal needs

FindLaw’s Learn About the Law features thousands of informational articles to help you understand your options. And if you’re ready to hire an attorney, find one in your area who can help.

Current as of January 02, 2025 | Updated by Findlaw Staff

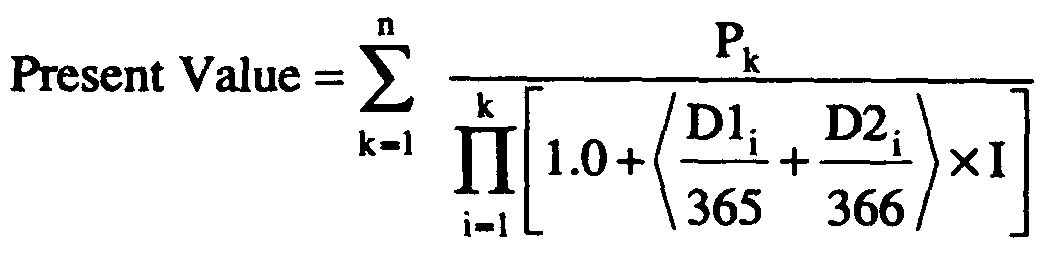

(a) The Discounted Present Value shall be calculated by RUS before prepayment is made by summing the present values of all remaining payments on all outstanding notes according to the following formula to compute the discounted present value of each note and adjusting as here and after provided for tax exempt financing.

Where:

Pk = Total payment, including interest, due on the kth payment date following the prepayment date.

n=Total number of remaining payment dates.

I=The discount rate applied to each transaction will be ascertained by using data specified in the “Federal Reserve Statistical Release” which is published each Monday. (See appendix B to subpart E of this part.) The specific discount rate will be the discount rate(s) specified in the “Treasury Constant Maturities” section of this publication eight working days prior to the closing. In applying the discount rate, the 1–year Treasury rate will be used for all notes with a remaining term of less than 2 years; the 2–year Treasury rate for notes with maturities between 2 and 3 years; the 3–year Treasury rate for all notes with maturities between 3 and 5 years; the 5–year Treasury rate for all notes with maturities between 5 and 7 years; the 7–year Treasury rate for all notes with maturities between 7 and 10 years; the 10–year Treasury rate for all notes with maturities between 10 and 30 years; and the 30–year Treasury rate for all notes with maturities longer than 30 years.

D1i = Number of days in the ith payment period that are in a non-leap year (365 day year).

D2i = Number of days in the ith payment period that are in a leap year (366 day year).

(b) Notwithstanding paragraph (a) of this section, in the event that the borrower shall elect to prepay using tax exempt financing, the calculation of the Discounted Present Value shall be adjusted to make the discount the equivalent of fully taxable financing.

Cite this article: FindLaw.com - Code of Federal Regulations Title 7. Agriculture § 7.1786.98 Discounted present value - last updated January 02, 2025 | https://codes.findlaw.com/cfr/title-7-agriculture/cfr-sect-7-1786-98/

FindLaw Codes may not reflect the most recent version of the law in your jurisdiction. Please verify the status of the code you are researching with the state legislature before relying on it for your legal needs.

Get help with your legal needs

FindLaw’s Learn About the Law features thousands of informational articles to help you understand your options. And if you’re ready to hire an attorney, find one in your area who can help.